The retail landscape in the United States is evolving rapidly, driven by changing consumer behavior and economic developments and technological advancements. Transaction data from millions of accounts reveal how spending preferences are shifting across various retail sectors.

In this analysis, we examined data for 300 retailer brands across 62 public companies in the US, covering big box, e-commerce, home improvement, department, specialty, discount, auto, footwear, and apparel. We explored seasonal spending patterns, market share dynamics, transaction frequencies, order values, and loyalty. The data is based on de-identified transactions that are sourced from credit and debit cards by Envestnet® | Yodlee® through partner financial institutions.

Overall trends show declining consumer confidence and economic uncertainty are impacting discretionary spending in the retail sector. The US economy is expected to experience slower growth in 2024, with inflation continuing to affect purchasing power. Consumer confidence has significantly declined (Figure 1), hitting its lowest point since July 2022. April 2024 marked the third consecutive month of falling confidence, with the index at 97.0, down from 103.1 in March 2024. Concerns about high inflation, interest rates, and modest GDP growth suggest potential signs of an approaching recession.

Volatility and recovery for retail spending

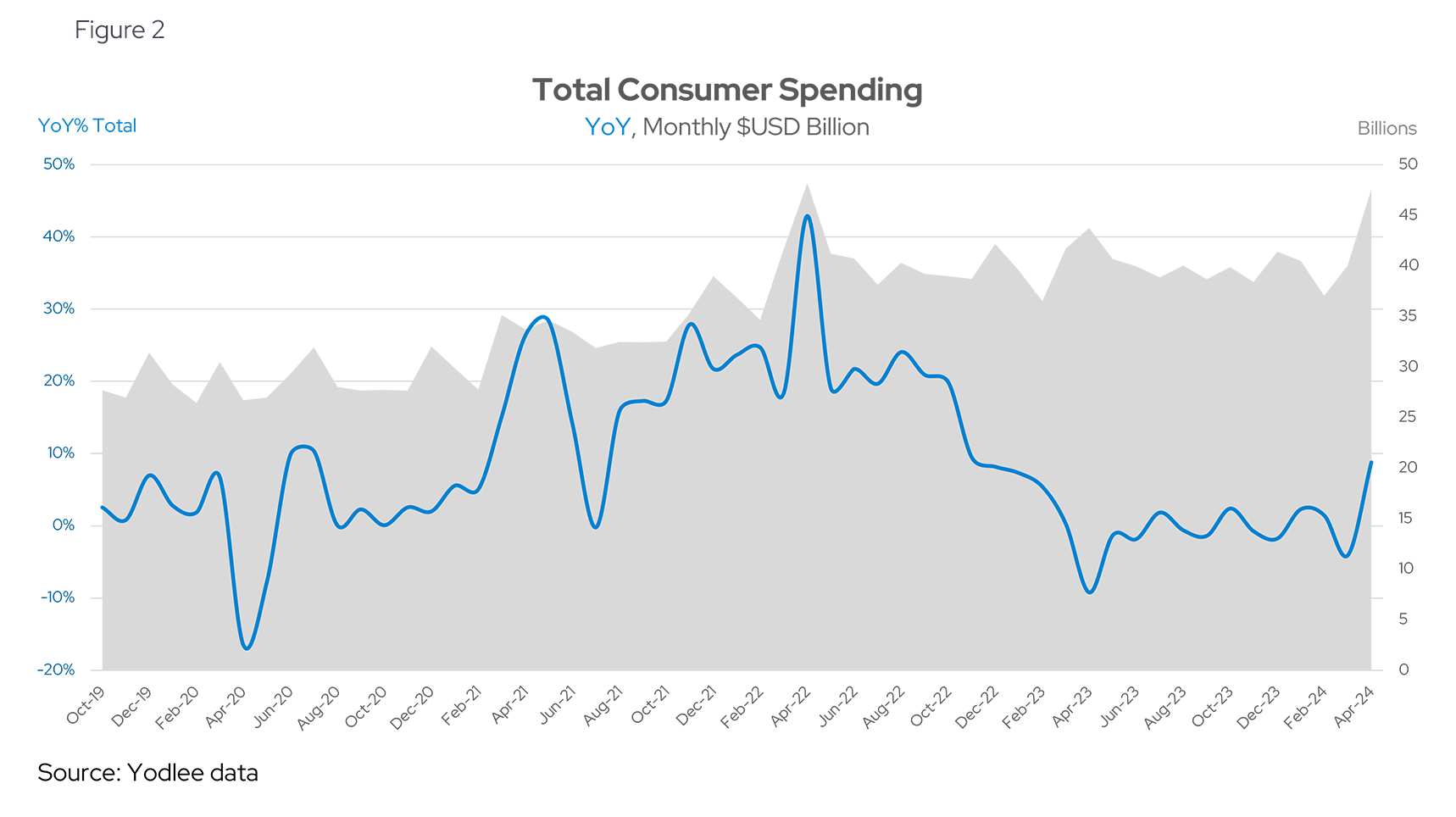

Retail spending dropped significantly in early 2020 due to the COVID-19 pandemic, with spend dipping as low as -18% year-over-year (YoY) (Figure 2) reflecting the immediate economic impact of lockdowns on the US consumer. By mid-2020, spending began to recover, reaching peaks in the spring of 2022, possibly driven by stimulus measures. But spending levels have remained relatively flat in the years since stimulus checks were discontinued. Inflation is baked into this aggregated spending number so we would expect the discretionary portion to have declined as total spend stayed relatively flat despite inflation.

Inflation eats into discretionary spending of US consumer

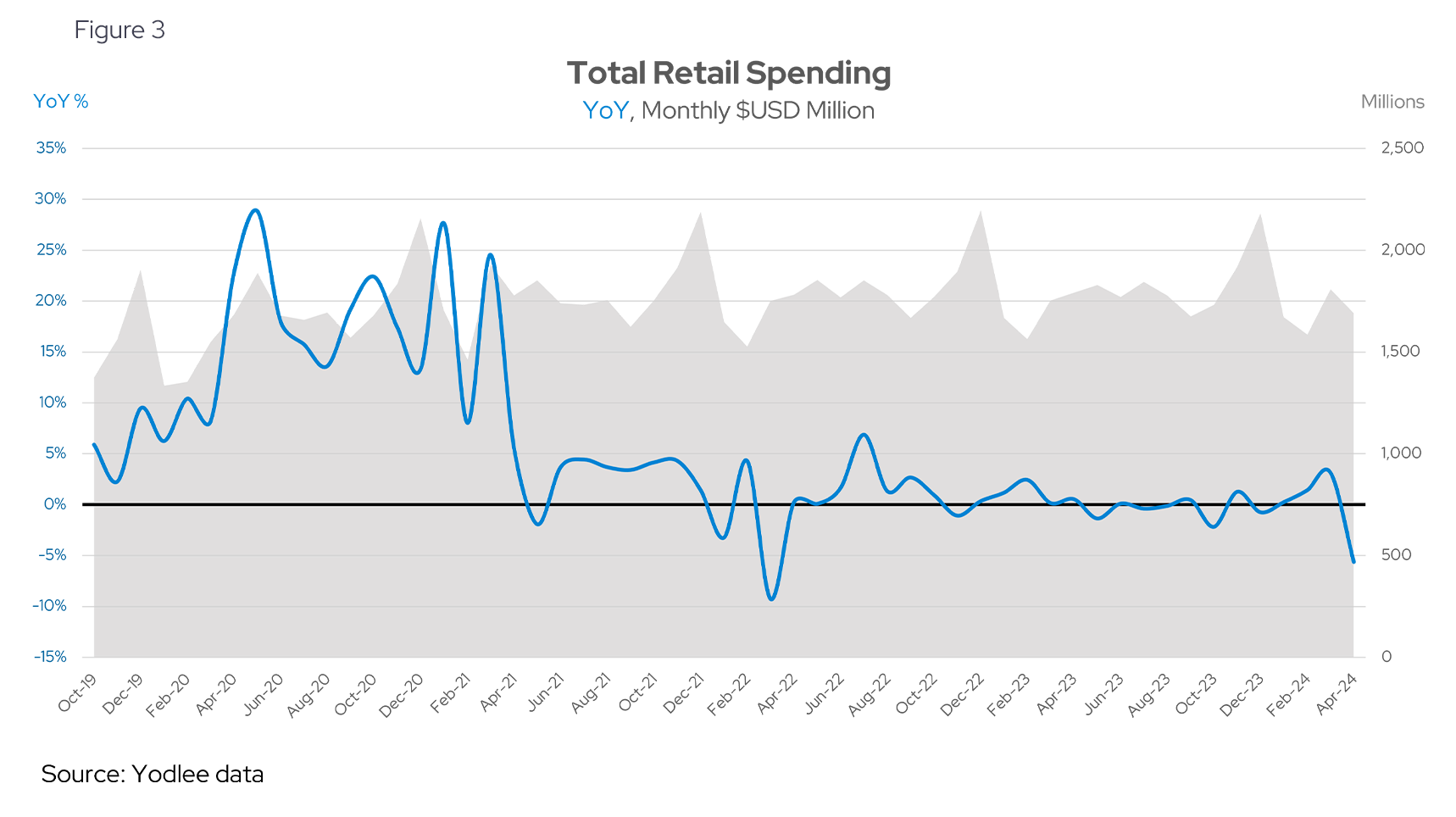

Indeed, the retail sector saw a sharp decline in YoY growth in 2020-21 and has not recovered since, spending a lot of time in negative territory in the past two years (Figure 3).

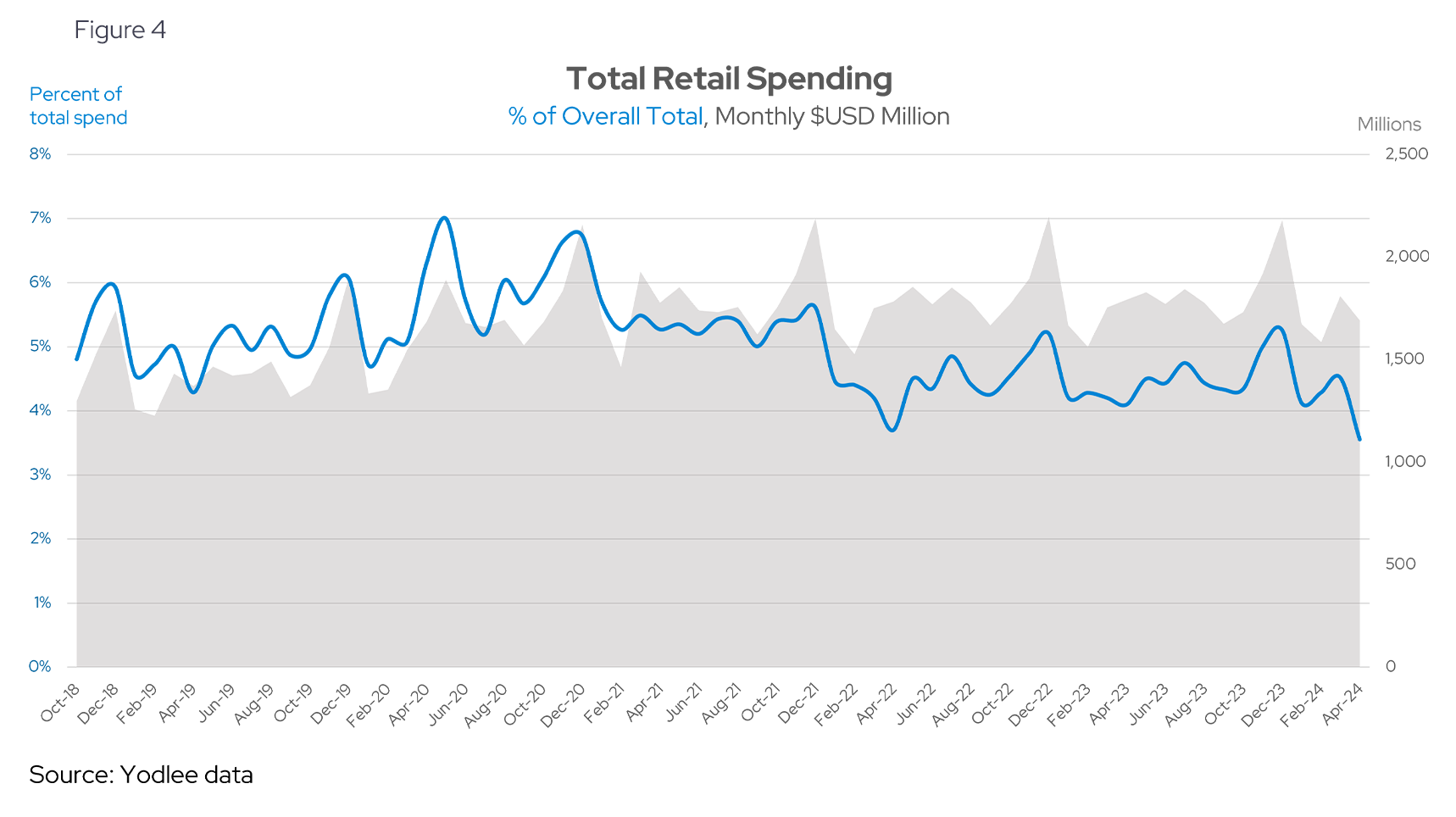

This disappointing growth is also evident in the percentage of total spend represented by discretionary spending. For example, before the pandemic, retail contributed around 5% to 6% of total spending. (Figure 4). At the height of the pandemic, this percentage dropped, reflecting a greater impact on retail compared to other spending categories.

The volatile recovery phase saw retail spending regain its share, but the notable decline in late 2022 and early 2023 implies that economic pressures affect discretionary retailers more than the rest. By early 2024, retail's share of total spending dropped below 4%, with April reaching its lowest value of 3.55% of total. (Figure 4). This highlights a shift in consumer behavior towards other spending categories, perhaps on staples as they demand a larger share of the wallet influenced by inflation.

Retail retreat: Consumer priorities are shifting

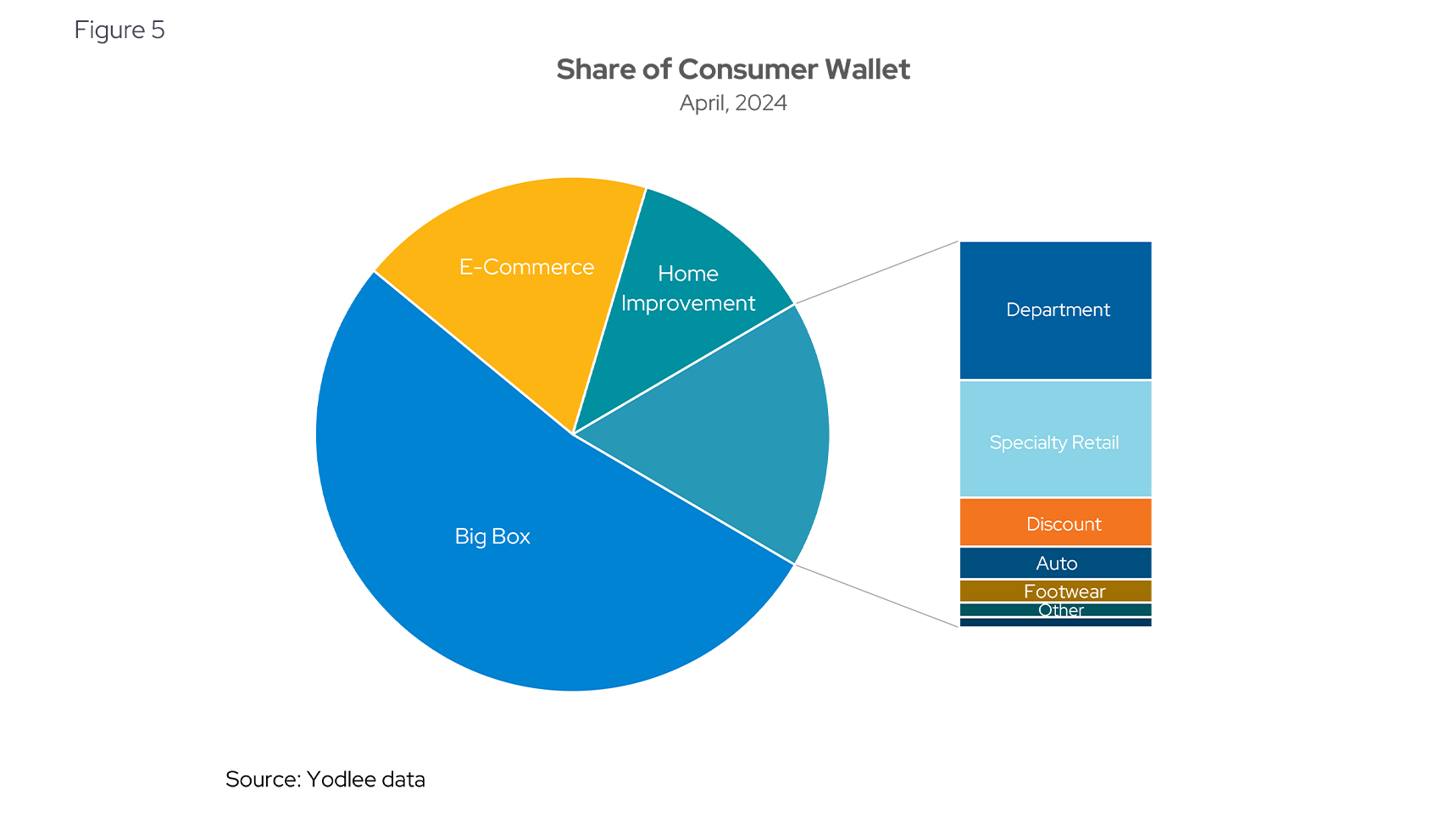

Given the clear divergence in consumer spend in retail versus total spend heading into the summer, it’s important to understand how retail spending is broken down and where consumer focus is headed. Figure 5 shows a snapshot of consumer spending in April 2024.

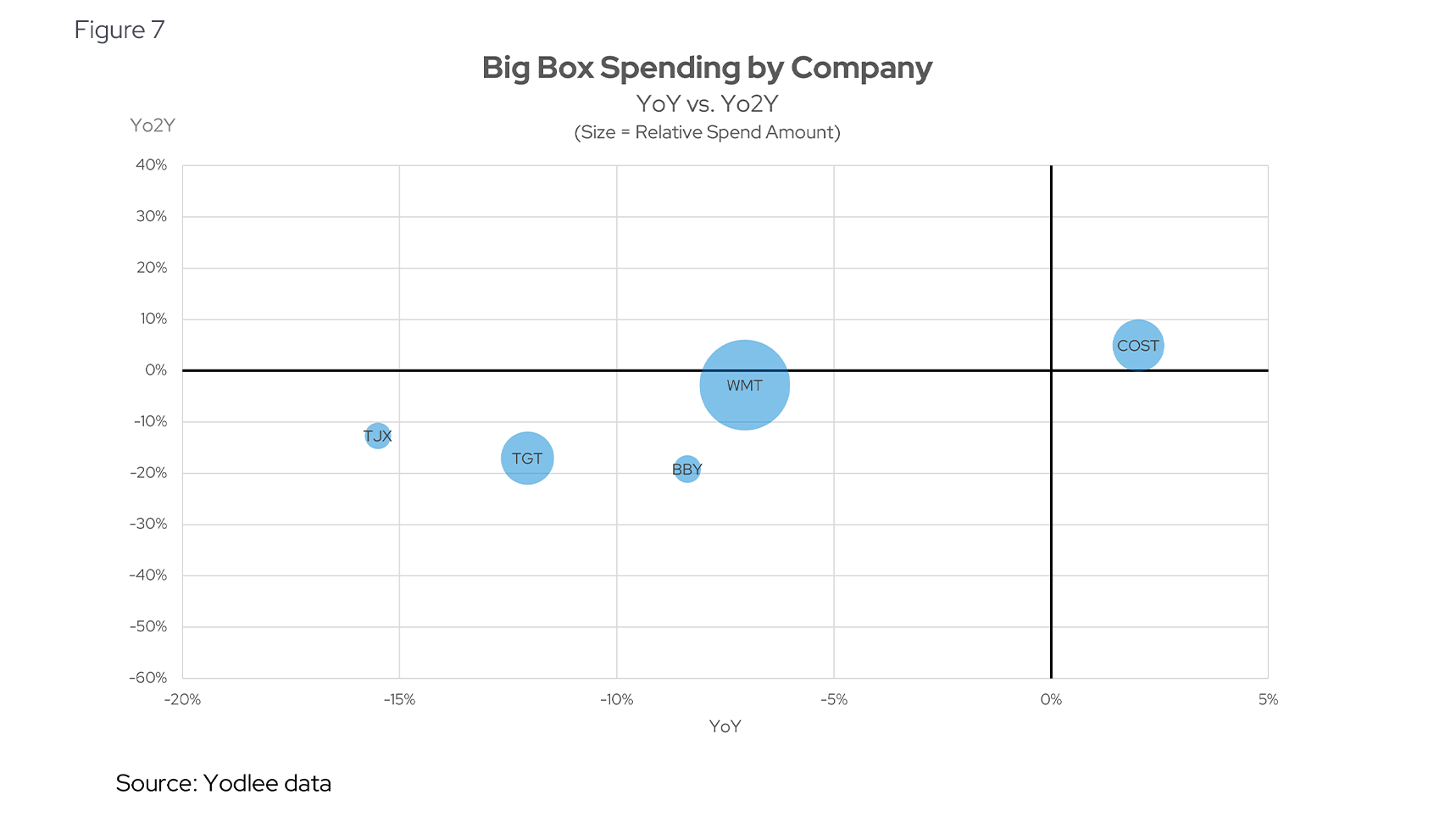

Big box retail is flat

The largest segment of consumer spending is directed towards Big box retailers. This category commands more than half of the US consumer’s wallet with a 53% share (Figure 5), indicating a strong preference for the convenience and variety offered by these large retail stores. Big box retailers typically provide a one-stop shopping experience, which continues to appeal to consumers looking for efficiency and competitive pricing.

However, it is important to note that the stability of this share of the wallet is not due to growth of the segment, but rather to the shrinking of other segments (besides e-commerce).

Major big box retailers show mixed performance, with Costco (COST) showing positive YoY and year-over-two-years (Yo2Y) growth potentially due to its strong value proposition and membership model. In contrast, Best Buy (BBY), Target (TGT), and TJX Companies (TJX) have experienced declines, reflecting challenges in maintaining consumer interest amid economic pressures and competition. Walmart (WMT), with a moderate Yo2Y decline, indicates resilience but is still affected by shifting consumer spending trends.

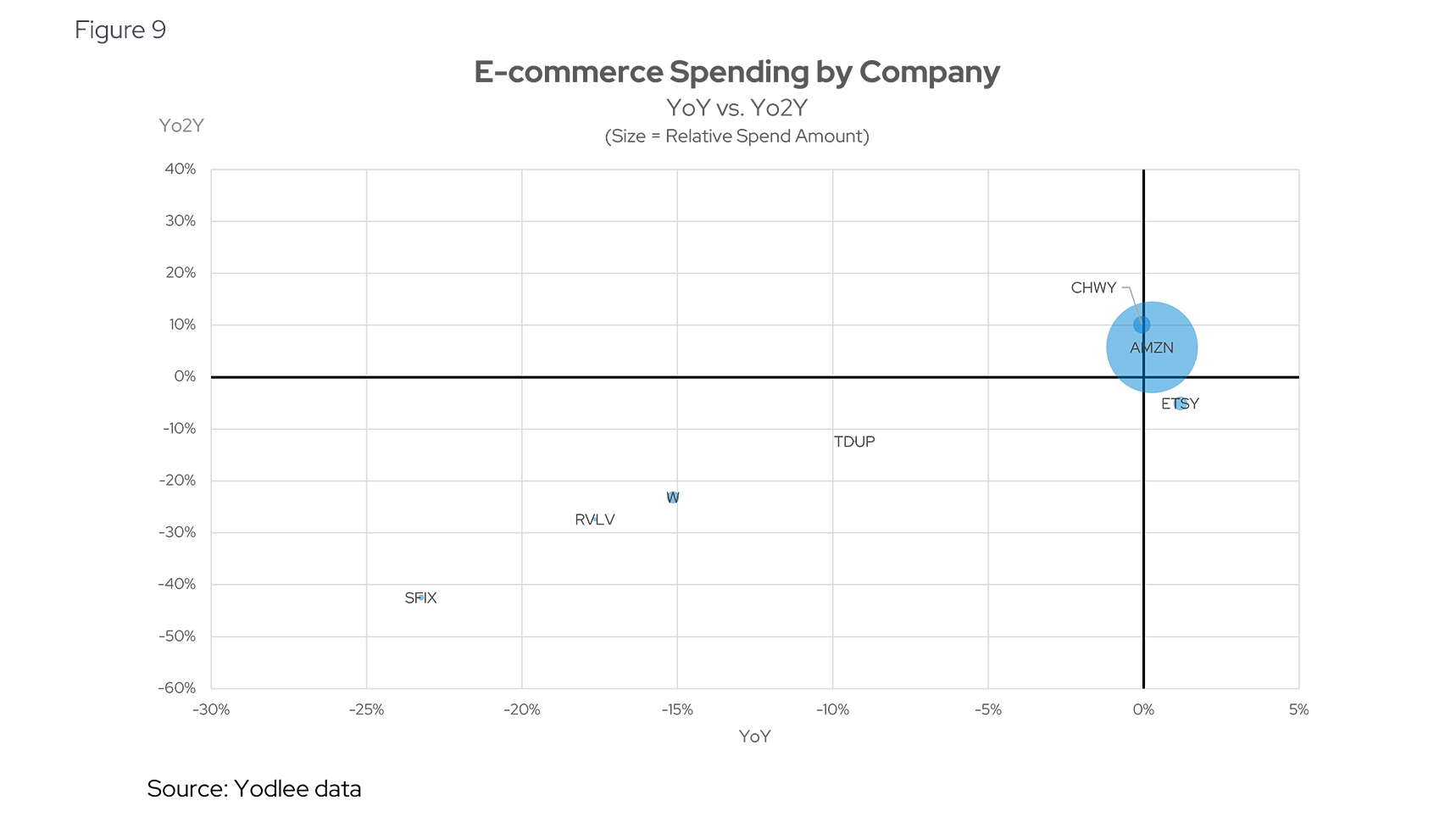

E-commerce is dominated by Amazon, which shows modest growth

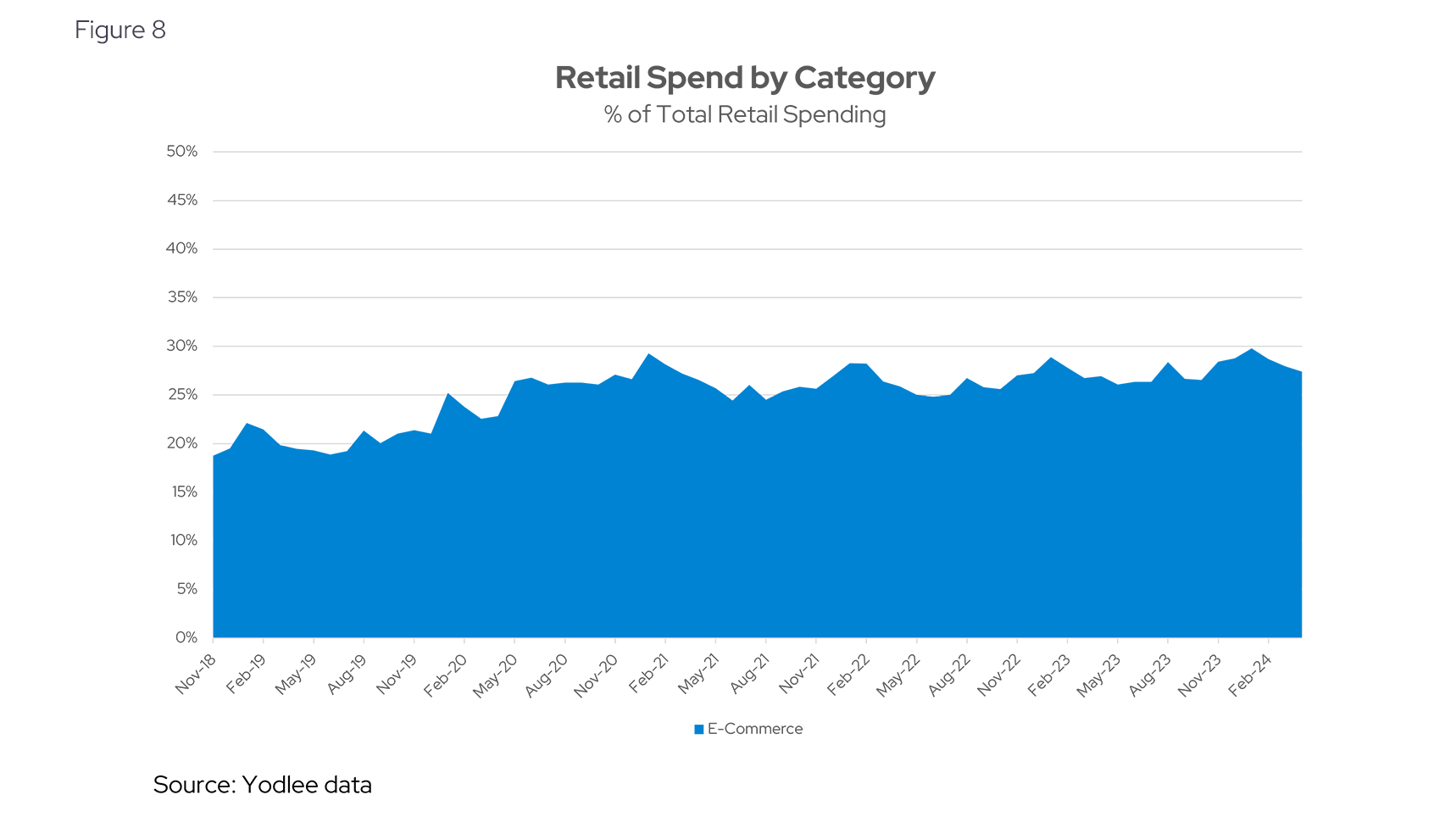

E-commerce remains a prominent category, occupying a significant and growing (figure 7) segment of the consumer wallet. Some drivers of online shopping include the convenience of home delivery, competitive pricing, and the vast selection available online. This relentless yet slow upward trend (seen clearly in Figure 7) underscores the importance of a robust online presence for retailers looking to capture market share in an increasingly digital age.

In e-commerce, Amazon (AMZN) remains in a dominant, while smaller and once-buzzy brands like Stitch Fix (SFIX) and Revolve (RVLV) have struggled to regain their pandemic-era performance. These smaller companies, which gained during the pandemic, are now facing challenges as consumers consolidate their spending towards larger, more established retailers. Amazon's performance should be viewed in the context of large-cap retail, distinct from the struggles of these smaller, single-brand marketplaces.

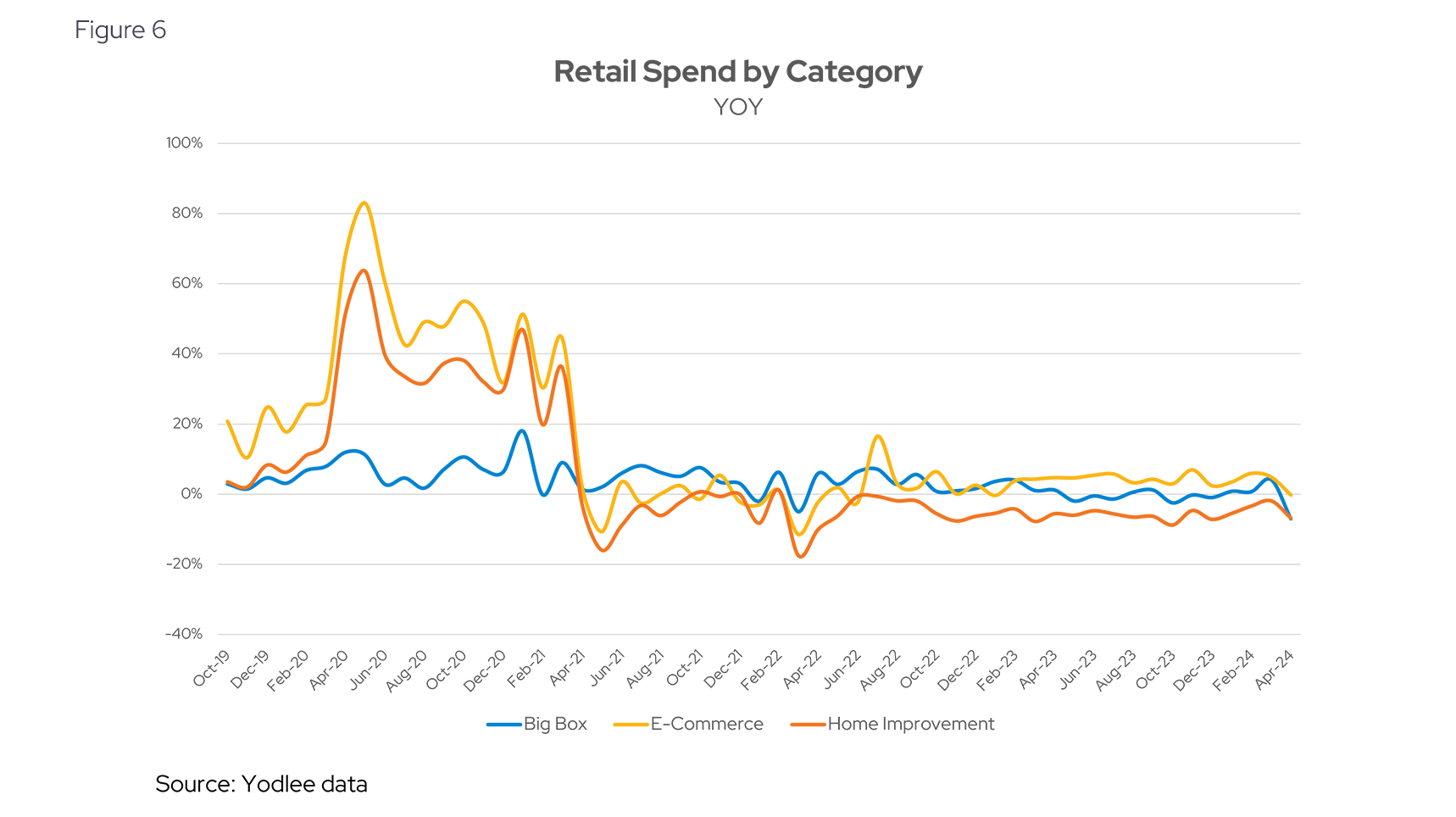

Home improvement is not what it used to be

Home improvement remains significant due to home-centric lifestyles, though demand for home improvement products and DIY projects. This trend, fueled by both ongoing home renovation projects and the rising popularity of gardening and outdoor activities, has slowed over the past few years as workers return to the office and home sales slow.

The seasonal nature of home improvement is illustrated in Figure 10, particularly around the pandemic in mid-2020. While both big box and e-commerce spike around the holiday seasons, home improvement receives most interest around the summer months.

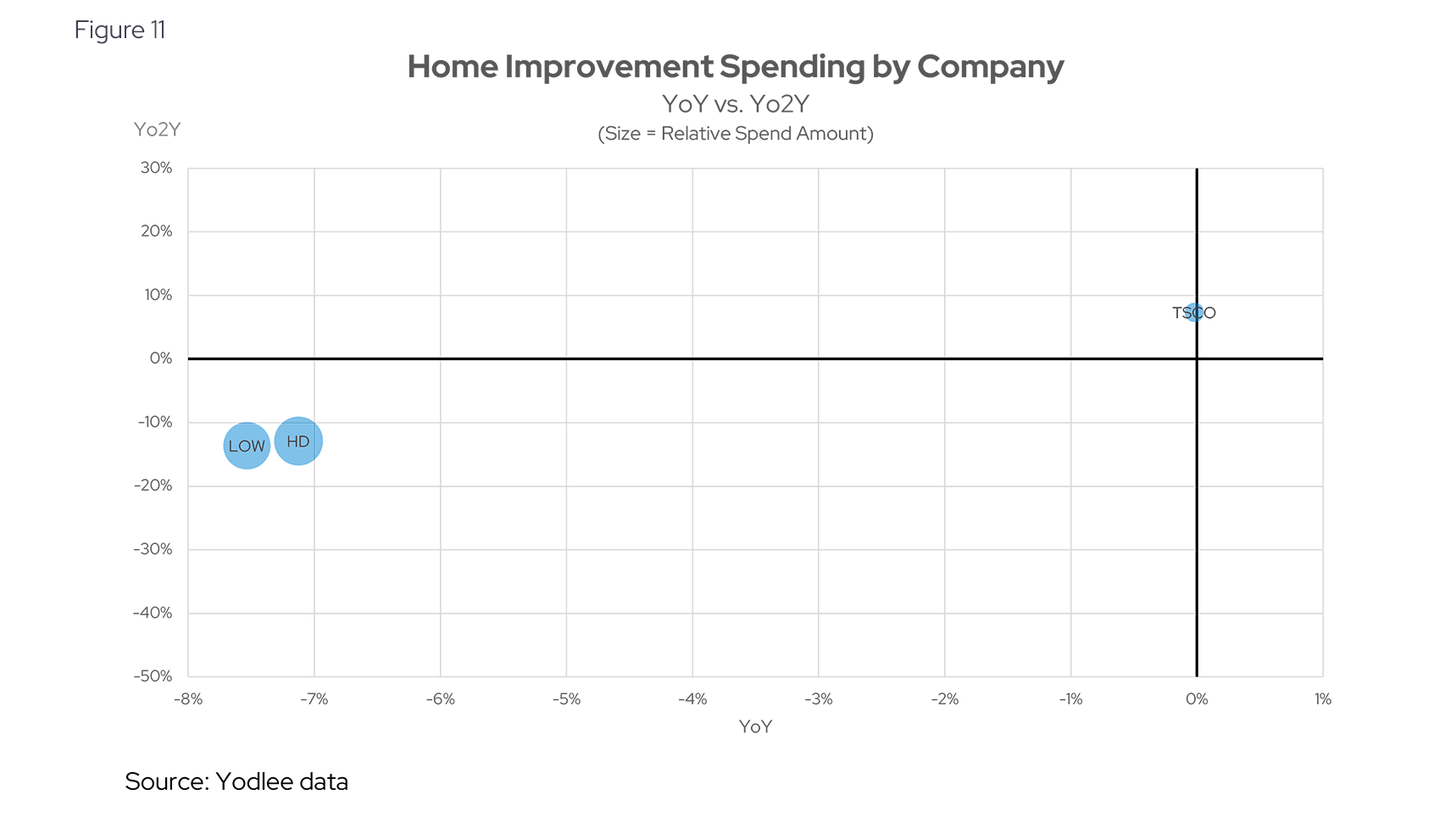

However, taking out the seasonality, it is evident that the segment is shrinking YoY (Figure 6). The two brands driving this downward trend are Lowes (LOW) and Home Depot (HD), with Tractor Supply (TSCO) managing to squeeze out modest Yo2Y growth (Figure 11) while staying flat YoY.

Notable developments in other categories

While big box, e-commerce, and home improvement certainly dominate consumer wallets, it’s worth noting key themes developing in other categories of retail:

- Apparel: Despite overall struggles, Levi Strauss & Co. (LEVI) posted slight growth, whereas Under Armour (UAA) and V.F. Corporation (VFC) faced substantial declines, highlighting broader challenges in the apparel category.

- Specialty retail: Abercrombie & Fitch (ANF) showed growth, while others saw declines, indicating varied performance in niche markets.

- Footwear: Boot Barn Holdings Inc. (BOOT) performed well, contrasting with declines from Crocs (CROX) and Nike (NKE), suggesting brand loyalty impacts success in this category.

- Auto: Advance Auto Parts (AAO) and AutoZone (AZO) faced declines, though less severe than other sectors, suggesting better positioning to weather economic fluctuations.

- Department stores: Ollie's Bargain Outlet Holdings Inc. (OLLI) showed strong performance, unlike traditional department stores like Macy's (M) and Kohl's (KSS), which struggled significantly.

- Discount retailers: Typically resilient, brands like Dollar Tree (DLTR) faced declines, indicating even cost-conscious consumers might be reducing spending or shifting to other channels.

Final thoughts for retail’s road ahead

The current retail landscape reflects significant consumer discretionary pressure, impacting various segments differently. Categories like specialty retail, along with certain e-commerce platforms, are underperforming possibly due to inflation reducing consumers' disposable income. In contrast, budget-friendly retailers such as Walmart, Dollar General, and wholesale clubs are generally holding up better. Big-ticket purchases are being deferred, explaining why Best Buy is struggling compared to other large box retailers. The data also highlights weaknesses in athleisure seen in the specialty retail and footwear categories (e.g., Lululemon, Nike). These trends illustrate the broader macroeconomic challenges and their specific impacts on different retail sectors with a few areas of stability or modest growth.

While consumer confidence remains low and retail is trending downward year over year, the data reveals a dynamic and evolving landscape, with consumer spending patterns leaning towards the convenience of e-commerce. Coming into the summer months, this trend will be one to follow as we see if home improvement can rebound and later how the holiday season takes shape for big box and e-commerce.

Want to see how transaction data can inform your investment process?

Learn more about Envestnet | Yodlee Merchant and Retail Insights and get a free demo from a sales representative.

About Envestnet Data & Analytics Income and Spending Trends

Envestnet Data & Analytics Income and Spending Trends utilize de-identified transaction data from a diverse and dynamic set of data from millions of accounts to identify patterns and context to inform spending and income trends. The trends reflect analysis and insights from the Envestnet | Yodlee data analysis team.