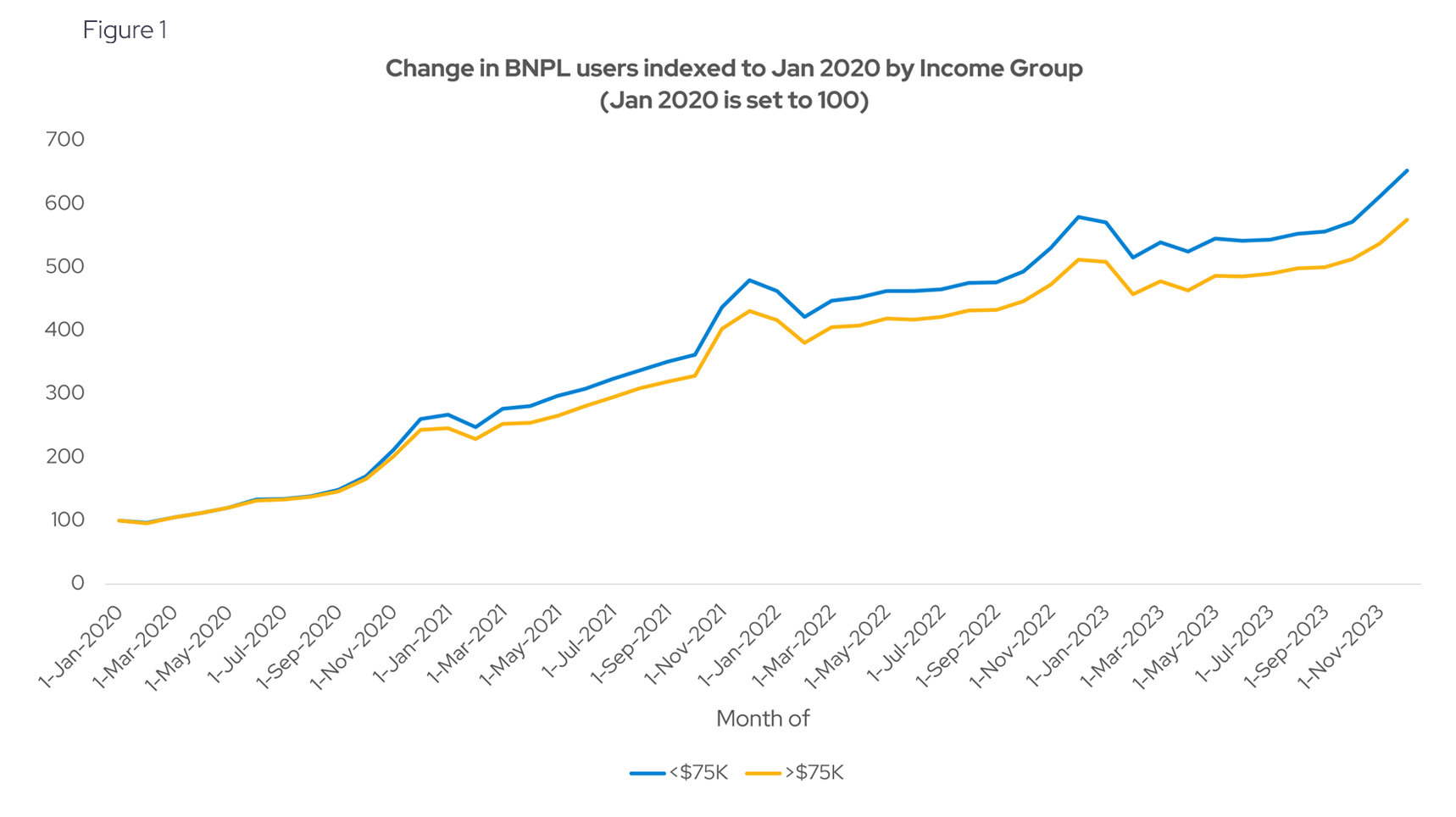

The lower income group uses BNPL more

Envestnet® | Yodlee® data shows that Buy Now, Pay Later (BNPL) services are more widely adopted among the lower income group (<$75K) while the higher income group (>$75K) has a lower representation of users (see Figure 1).

This is in alignment with a report from the Federal Reserve that stated consumers with a household income of less than $75,000 are four times more likely to use BNPL services than those with a household income above that threshold. The report also shows that BNPL users are generally lower earning, younger, and non-White compared to other payment tools.

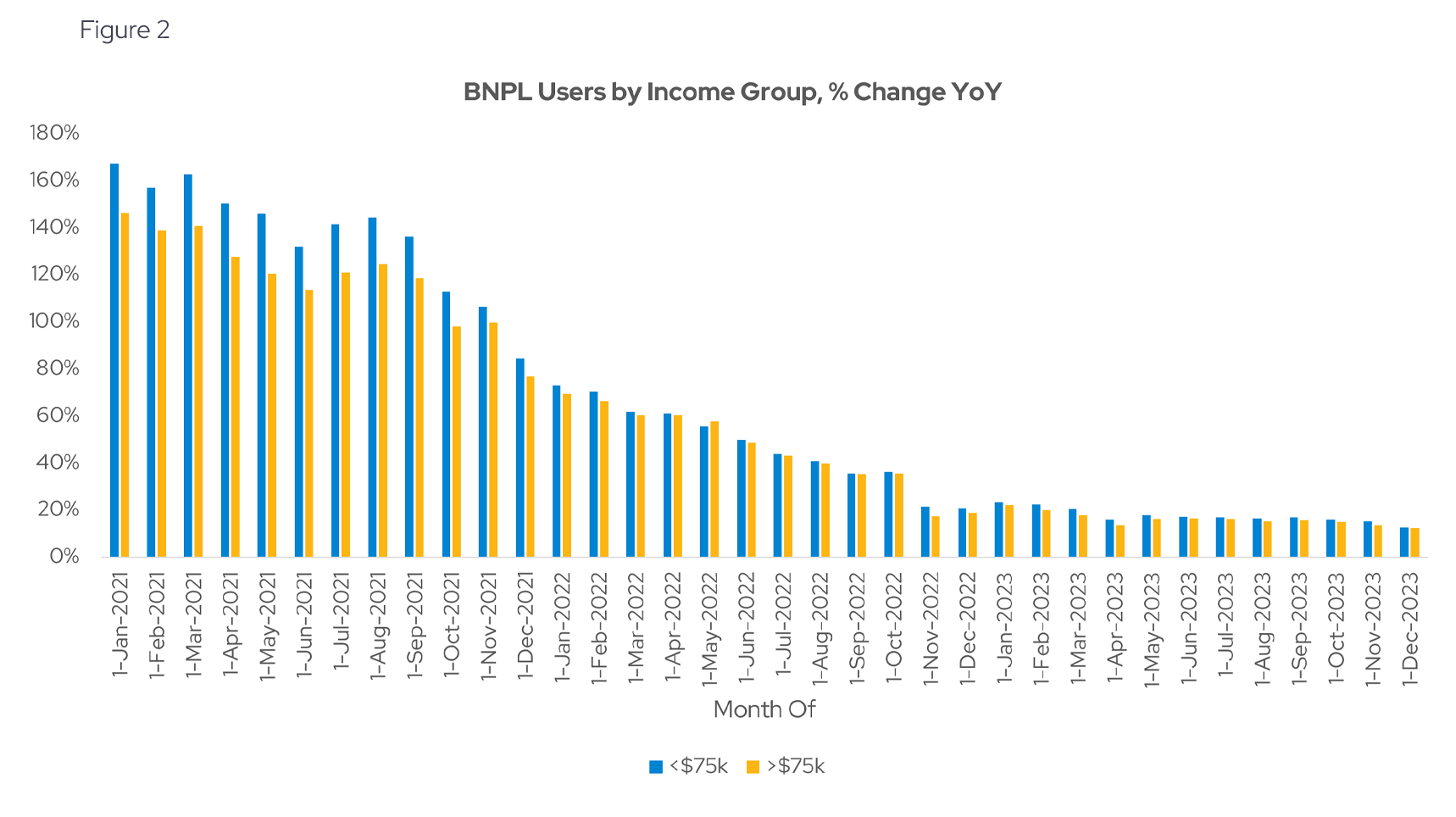

BNPL user base is more steady in 2023

Yodlee data suggests that the rapid surge in BNPL adoption observed in 2020 has tapered off, leading to a more consistent and steady user base growth from 2023 onwards for both lower income earners (<$75K) and higher income earners (>$75K) (see Figure 2).

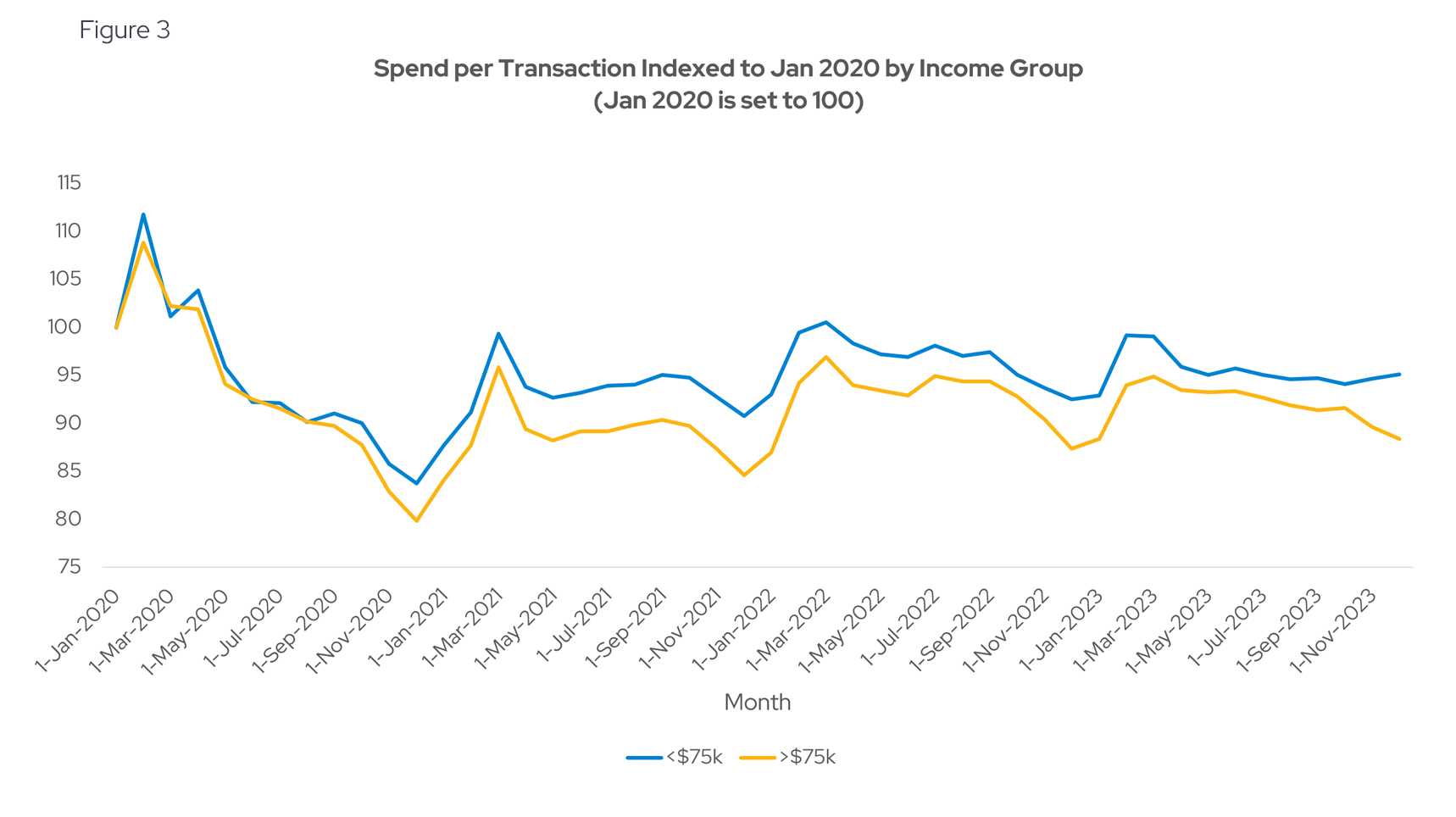

Lower income group spent more per transaction

Yodlee data suggests that the lower income group (<$75K) tends to spend more per transaction when utilizing BNPL services compared to the higher income group (>$75K). The lower income group is potentially making fewer but higher value transactions compared to the higher income group.

According to a report from Bankrate, the average amount financed among BNPL borrowers within a year is $1,000. Easier payments, greater flexibility, and saving on interest were among the top three reasons consumers choose to use a BNPL to finance their purchase.

While many BNPL borrowers don’t exhibit noticeable indications of financial stress due to the actual product, a 2023 CFPB report found that they’re more likely to experience financial stress than non-borrowers. It also found borrowers are active users of other credit products and loans and are more likely to experience financial distress than non-borrowers.

Want to get ahead of consumer spending trends?

Subscribe to our research data blog for ongoing updates or reach out for a personalized, up-to-date view of Yodlee consumer spending data.

About Envestnet | Yodlee Merchant, Retail, Shopper, and Spend Insights

Envestnet | Yodlee Merchant, Retail, Shopper, and Spend Insights utilize de-identified transaction data from a diverse and dynamic set of data from millions of accounts to identify patterns and context to inform spending and income trends. The trends reflect analysis and insights from the Envestnet | Yodlee data analysis team. By combining data with intelligence – connecting vast amounts of actual de-identified shopping data with state-of-the-art analytics and machine learning – Envestnet | Yodlee provides visibility into a large set of shopping daily purchase behavior including, but not limited to, transactions, customer lifetime values, and merchant/retailer shares.

To learn more about Envestnet | Yodlee Merchant and Retail Insights and get a free demo, please contact an Envestnet | Yodlee sales representative.